Approaches to the Computation of Working Capital (with Numerical problems)

Working Capital Approaches

Working capital measures a company's operational efficiency and short-term financial health. It is calculated as the difference between current assets and current liabilities. Various approaches to computing working capital offer insights into different aspects of financial management:

- Net Working Capital Approach

- Gross Working Capital Approach

- Working Capital Cycle Approach

1. Net Working Capital Approach

Net working capital (NWC) measures a company’s liquidity and its ability to meet short-term obligations with short-term assets.

Formula:

Example: Consider a company with the following balance sheet items:

- Cash: $20,000

- Accounts Receivable: $50,000

- Inventory: $30,000

- Accounts Payable: $40,000

- Short-term Loans: $10,000

Net Working Capital = (20,000+50,000+30,000)−(40,000+10,000) = 100,000−50,000 = 50,000

The company’s net working capital is $50,000.

2. Gross Working Capital Approach

Gross working capital refers to the total of all current assets. This approach focuses on the firm’s investment in short-term assets, emphasizing the company’s ability to cover its short-term financial needs.

Formula: Gross Working Capital=Total Current Assets

Example: Using the same balance sheet items from the previous example:

Gross Working Capital

=20,000+50,000+30,000=100,000

The company’s gross working capital is $100,000.

3. Working Capital Cycle Approach

The working capital cycle (WCC) measures the time it takes for a company to convert its net working capital into cash. It is an important indicator of operational efficiency.

Formula: WCC = Inventory Period

+Receivables Period−Payables Period

Where:

- Inventory Period: The average time inventory is held before sale.

- Receivables Period: The average time to collect receivables.

- Payables Period: The average time to pay suppliers.

Example: Suppose a company has the following average periods:

- Inventory Period: 30 days

- Receivables Period: 45 days

- Payables Period: 25 days

WCC = 30+45−25 = 50 days

The company’s working capital cycle is 50 days, indicating it takes 50 days to convert its working capital into cash.

Numerical Problems

Problem 1: Net Working Capital Calculation

Scenario: A company has the following current assets and liabilities:

- Cash: $15,000

- Accounts Receivable: $25,000

- Inventory: $35,000

- Accounts Payable: $20,000

- Short-term Loans: $5,000

- Accrued Expenses: $10,000

Solution: Net Working Capital=(15,000+25,000+35,000)−(20,000+5,000

+10,000)=75,000−35,000=40,000

The company’s net working capital is $40,000.

Problem 2: Gross Working Capital Calculation

Scenario: A company’s current assets include:

- Cash: $10,000

- Accounts Receivable: $20,000

- Inventory: $15,000

- Marketable Securities: $5,000

Solution: Gross Working Capital

=10,000+20,000+15,000+5,000=50,000

The company’s gross working capital is $50,000.

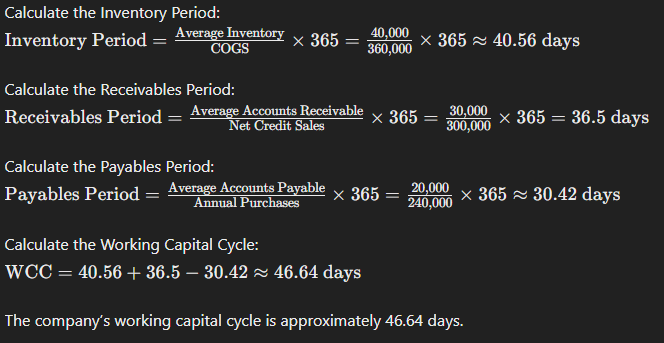

Problem 3: Working Capital Cycle Calculation

Scenario: A company’s financial data shows:

- Average Inventory: $40,000

- Cost of Goods Sold (COGS): $360,000

- Average Accounts Receivable: $30,000

- Net Credit Sales: $300,000

- Average Accounts Payable: $20,000

- Annual Purchases: $240,000

Solution: